The COVID-19 pandemic has had a devastating impact on many small businesses. Many business owners are seeking financing in order to survive this difficult time.

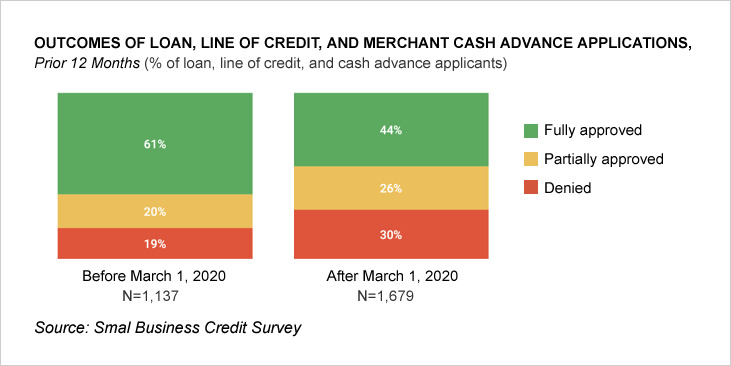

Small business owners may not be the best candidates for loans. The Federal Reserve Banks’ latest Small Business Credit Survey revealed that approval rates for merchant cash advances, small business loans and credit lines all decreased after the outbreak of the flu pandemic.

Before March 2020, only 61% of applicants received a full approval of the loan that they applied for. 20% of applicants were partially approved and 19% denied. When the pandemic began, only 44% were approved fully, and 26% were approved partially. The remaining 30% were rejected.

There are many reasons why your small business loan application was denied.

The most common reasons why small businesses are denied financing

Before you reapply, you must identify the reasons why you were rejected for a small-business loan. Here are the top reasons why applicants are rejected:

1. You have a bad credit rating

Credit scores for both your personal and business are important in any small business funding you apply. Your credit score is an indication of your ability repay debts and pay monthly recurring expenses.

The NSBA Small Business Access to Capital Study found that 20 percent of small business loans were denied because of poor credit. A 2015 American Dream Gap study found that 45% small business owners did not even know they had business credit scores, and 72% didn’t know where to get information on them. Eighty-two percent of small business owners do not know how their credit score is calculated.

If you think your credit rating is the reason for your denied loan application, you should revisit your a data-feathr-click track=”true” data-feathr link aids='[“5efb8bc85e7bae85c61251d6″]’ href=”https://www.smbcompass.com/sba/loan/creditscoreminimum/”. You should review your score to see what factors contributed to your loan application being denied.

2. You’re in the wrong industry

Many business loan applications are denied due to their nature. This is unfair. Some industries were more severely affected than others by the pandemic.

S&P Market Intelligence determined that the five industries most likely to be affected by this pandemic were: Airlines, oil and gas drilling companies, restaurants, auto equipment and parts, and leisure facilities. It is possible that your business falls into one of these categories.

Small businesses, by their nature, are considered a high-risk investment for traditional lenders such as banks and credit unions. You can compensate if you think this is an issue for you by having a high credit score or presenting your long-term plan.

3. You are not spending enough time on your business

Traditional lenders tend to view new businesses as having not been around long enough to establish a credit history. Before a business can be granted a loan, it must have a track record of consistent payment for three to five years.

You can use your personal credit to prove your creditworthiness if your business is new. You can put up collateral as well to reduce the risk for the lender.

Traditional lenders often reject small businesses that haven’t been in business for three years. You might consider alternative financing, which doesn’t require you to have been in business for a certain number of years.

4. You have either a low or high debt utilization.

Some lenders want to see that you are using your credit. Why? Your lender will not be able to see that you can pay back a debt if you have had credit for a very long time. A healthy credit history would be needed to support your loan application.

They also don’t like to see you overusing your credit, because this could indicate that you are a high-risk borrower. Ideal is to maintain a credit usage ratio of 30%. If you have a credit limit of $100,000 on your business card, you should keep the usage to around $30,000.

Keep track of all of your accounts, and ensure that your debt usage is acceptable to your lender.

5. You don’t possess a solid business strategy

A lack of a sound business plan is another common reason why small business owners are rejected for loans. Small businesses, as mentioned above, are more risky loan applicants because they have less stability in their income and fewer resources available to support growth.

You can assure your lender that you will be able to pay back your loan by presenting a solid business plan. You can show your lender that your company has a clear direction for growth, which will give them confidence that you won’t default on your loan before it’s due.

Cash flow statements are also required to demonstrate to lenders the amount of money flowing through your business. Even though small businesses are profitable, they may struggle to balance the books because they pay their suppliers in advance before receiving their customers’ payment.

How to Get Approved for Financing

Don’t give up hope if you have been rejected for a loan. You can still apply for financing with the same lender, or a different one. Build your credit score for both personal and business purposes to be approved for a small-business loan. You must have a minimum of 600 points for your personal credit and 75 points for your business.

Find a lender that specializes in your field and maintain your debt usage at the desired level. Do not close your accounts, even if you aren’t using them. This will negatively affect your credit rating.

Bottom Line

Denied a loan can be devastating, especially if you are in a hurry to get the money. You should review your documents with your lender to improve your chances of obtaining a small business loan the next time.